Une manière de réduire les émissions de gaz à effet de serre (GES) consiste à identifier un prix du carbone efficient, c’est-à-dire qui puisse être utilisé pour transférer le coût des externalités négatives des GES vers les entreprises qui en sont responsables, afin de les inciter à les éviter ou au moins à les réduire par des investissements appropriés. Cependant, une hausse du prix du carbone peut affaiblir financièrement certaines des entreprises concernées, et par extension les banques auxquelles elles ont emprunté. Dans ce contexte, la Banque Centrale Européenne a organisé un stress test climatique, dont le risque lié à une hausse du prix du carbone constitue une composante. Dans cet article qui résume leur publication sur ResearchGate, les auteurs présentent une méthode pratique d’estimation de la sensibilité du risque de crédit au prix du carbone.

Abstract. One way to reduce greenhouse gas (GHG) emissions is to find an efficient carbon price, one which can be used to transfer the cost of the negative externalities of GHGs to the companies that are responsible for them, which can then avoid or reduce them through appropriate investments. However, a rising carbon price may financially weaken some of the companies concerned, and by extension the banks they borrowed money from. In this context, the European Central Bank has organized a climate stress test, part of which concerns the risk related to a rise in the price of carbon. In this paper, we present a practical method for assessing the sensitivity of credit risk to the carbon price.

Introduction

In a context of climate change due to human activities, one of the major indicators of the ecological transition, which has also become a tool for steering the politics of change, is the quantity of greenhouse gases (GHGs) emitted by economic activities. Recent international agreements, such as the Paris Agreement, have set GHG emission targets for the international community, and for particular countries through nationally determined contributions (NDCs). These NDCs are roadmaps that countries commit to follow in order to reduce their GHG emissions.

Two-thirds of the NDCs filed by countries include the implementation of a carbon price as a tool to control or offset GHG emissions. The objective of a carbon price is to make emitters pay the cost of the externalities induced by GHGs. This idea existed prior to the Paris Agreement: since 2005 and the implementation of an emissions trading scheme (ETS) within the European Union (EU), carbon has a market price.

Recently, the climate and regulatory context has led to an inflationary carbon market. For banks, credit risk exposure may be sensitive to increases in the carbon price, with risks ranging from asset value impairment to obligors’ default. This risk belongs within the sphere of climate transition risks. Like macro-financial risks, transition risk is therefore of interest to banking regulators.

In this context, the European Central Bank (ECB) has decided to organise a climate risk stress test (CST), inspired by the stress tests of the European Banking Authority (STEBA) for macro-financial risks. For this exercise, the ECB drew on the climate scenarios of the Network for Greening the Financial System (NGFS) and defined a set of macro-financial trajectories including the impacts of climate change. In these scenarios, a short-term transition risk corresponds to a sudden and unexpected increase of the carbon price by USD100 per ton. It is then necessary for banks to have new and clear methodologies to address this risk, ones which can be plugged into their internal credit risk models.

In this paper, we focus on estimating the sensitivity of credit counterparties’ probabilities of default (PDs) to an increase in the carbon price.

GHG emissions and the carbon price

GHG emissions are divided into three scopes. Scope 1 (S1) covers emissions from fixed and mobile installations within the organisational perimeter, emitted directly by the production activity. Scope 2 (S2) includes indirect emissions associated with the production of electricity, heat or steam imported for the organisation’s activities. Scope (S3) includes all other emissions indirectly related to the activity before or after production.

The carbon price is an instrument that takes into account the negative externalities of GHG emissions. These include crop damage, healthcare costs related to heat waves, droughts and pollution, property losses due to flooding and sea level rise, etc. GHG emitters must then decide whether it is more profitable to pay a carbon price or to reduce their emissions through appropriate investments and transformations.

Credit risk and the carbon price

Credit risk is defined as the risk that a borrower will not be able to meet its financial obligations on time. Considering that the carbon price is an additional cost for companies, we may assume that the creditworthiness of at least some companies will suffer from carbon price inflation. The difficulty is to estimate the sensitivity of their creditworthiness to changes in the carbon price. With methodological elements similar to those of bank-specific stress tests, we compute this sensitivity with a practical method which can be implemented by banks using their internal credit risk models, and which meets the requirements of the ECB’s CST.

Our methodology

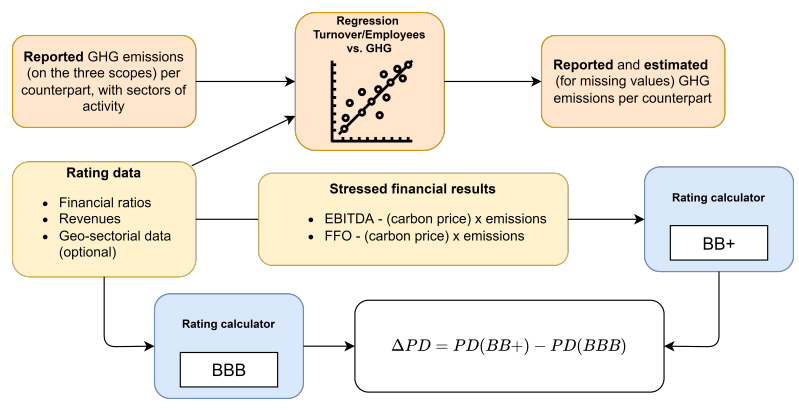

It consists of three main steps summarized in Figure 1 :

- First, we gather data required to compute the probability of default (PD) of each company, and their GHG emissions. For the companies that do not report their GHG emissions, we use a calculation based on energy consumption, turnover or number of employees to estimate missing GHG data.

- Then, we stress financial variables (EBITDA, FFO, net debt, interest, etc.) present in PD models with carbon costs.

- Finally, we compute a rating (or associated PD) before and after the carbon stress. For the current analysis, we have applied this method on 1,200 European companies, from many sectors and with several initial credit quality levels.

To compute the PD before and after the carbon price shock for all companies, we use a financial rating model based on the following credit ratios: net debt-to-EBITDA, EBITDA interest coverage, EBIT interest coverage, and funds from operations (FFO) to net debt. We note that any rating/PD model can be stressed using additional costs, and in particular any carbon cost.

To obtain GHG-based stressed PDs, we impact the four credit ratios with additional carbon cost, for each firm. As with the ECB’s CST short-term transition risk, we assume that the balance sheet is static, that there is no passing on of the carbon price to customers or suppliers, and that there is no sectoral collusion to reduce or share the impact of a high carbon price.

Figure 1: Diagram of the complete methodology for assessing the sensitivity of PDs to the carbon price. Orange boxes are for GHG emissions data. The yellow boxes refer to the rating data. The blue boxes correspond to the rating before and after carbon stress. The white box quantifies the stress applied to PDs

Portfolio-level analysis

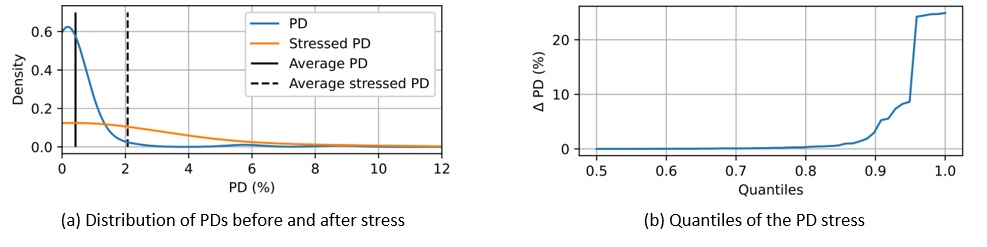

We show in Figure 2 (a) the distribution of the density of the PDs before and after the carbon price rise. While they were largely contained in a range between 0 and 2% initially (blue curve), the PDs then move into a range between 0 and 8% (orange curve) after the carbon shock. The average PD is multiplied by more than 4, going up from 0.43% to 2.07%. The evolution of the quantiles of the difference between stressed and unstressed PDs in Figure 2 (b) shows that the majority of the impact is concentrated in ∼10% of the companies with a significant increase in PDs, sometimes one higher than 20%.

Figure 2: Elements of the PD distribution before and after carbon stress. In Figure 2a, the respective pre- and post-stress averages are 0.43% and 2.07%.

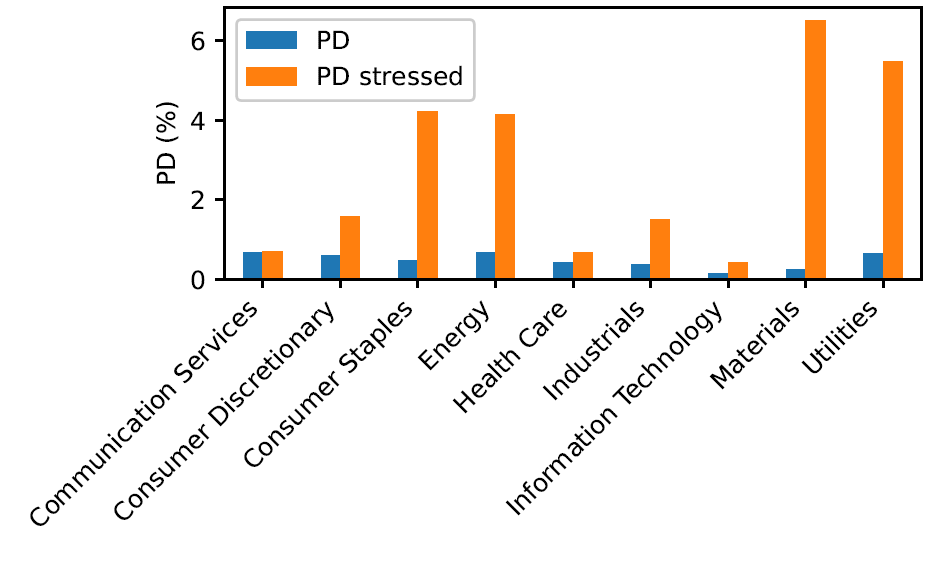

Figure 3: Mean PD (%) before and after stress related to carbon price

Sector-level analysis

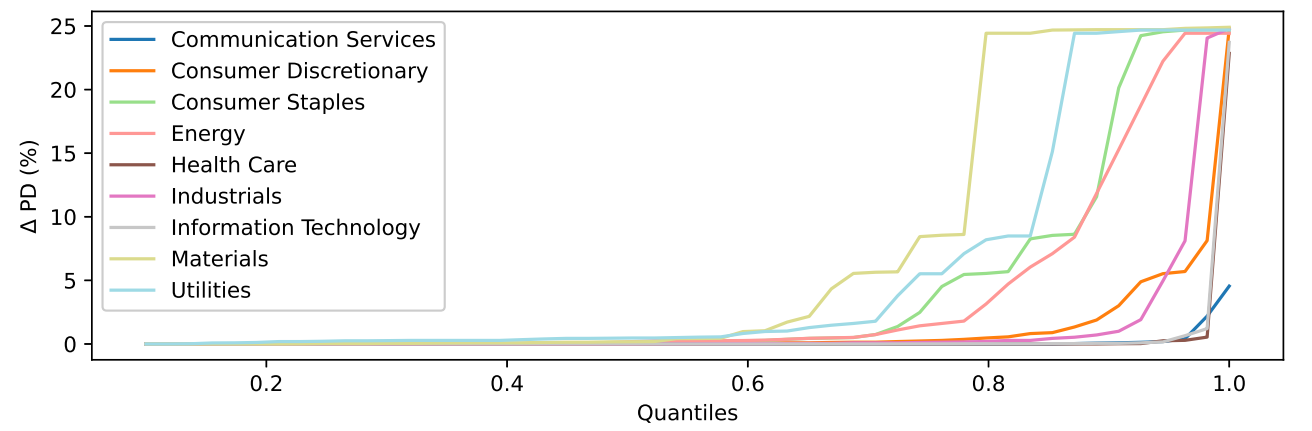

In Figure 3, we observe that Materials, Utilities, and Consumer Staples are the most impacted sectors. We can break down the analysis by looking at the quantiles of the difference between stressed and unstressed PDs in Figure 4. We see that the creditworthiness of the Materials sector deteriorates the fastest, with ∼35% of companies having a greater than 5%. For Utilities, the average degradation of 5% concerns ∼20% of the companies. It is directly followed by Consumer Staples and Energy.

Figure 4: Quantiles of by sector.

Conclusion

In this article, we have proposed a practical methodology for banks to assess the resilience of their obligors to a sudden and sharp increase of the carbon price of USD100 per ton, as requested in the ECB’s CST. We have shown that the average PD of the portfolio would be multiplied by 4, going up from 0.43% to 2.07%, with the large majority of this impact being concentrated in the Materials, Utilities, Consumer Staples, and Energy sectors.

Mots-clés : Émissions de gaz à effet de serre – Risque de transition – Risque de crédit – Stress test climatique BCE.

Lien vers l’article complet en français => (PDF) Sensibilité des probabilités de défaut au prix du carbone (researchgate.net)

Lien vers l’article complet en anglais => (PDF) Sensitivity of Probabilities of Default to Carbon Price (researchgate.net)

Rémy Estran-Fraioli (PhD) is Head of Modelling & Analytics at EthiFinance. He is a graduate of ESCP Business School, Mines ParisTech (2012), and holds a Master from Université Paris X and a Doctorate from Université Paris 1 Panthéon-Sorbonne (2020).

Lucie Delzant is a Consultant in Responsible Investment at EthiFinance. She holds a Master from Université Paris 1 Panthéon-Sorbonne (2018) and a Master from ESCP Business School (2020).

Elie Hériard-Dubreuil, ENSAE (2000), is President at EthiFinance

- Sensitivity of Probabilities of Default to the Carbon Price - 15 septembre 2022