Cet article est une version légèrement condensée de celui publié sur le site de recherche d’Amundi

The social bond market is developing, offering new investment opportunities

The Covid-19 crisis has placed new themes and topics under the financial world’s spotlight. Remarkably, it has highlighted the importance of integrating social risks into investment decisions and brought about significant opportunities for investors.

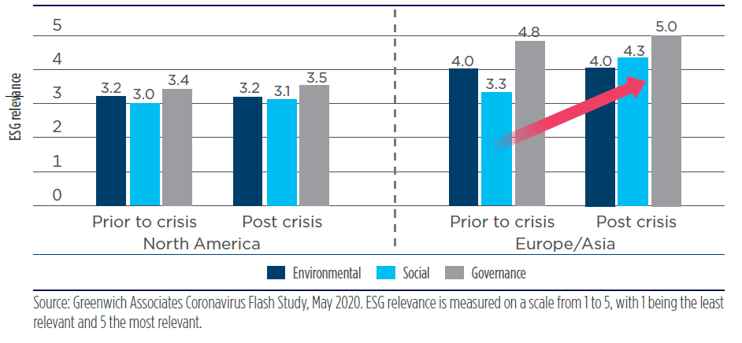

In fact, in North American markets, the social pillar – which had been lagging behind the environmental and governance pillars in previous years – outperformed the other two in the first quarter of 2020.[1] Also, while the perceived relevance of the environmental and governance factors has not changed much as a result of Covid-19, institutional investors in Europe and Asia have recently reported to give a much greater importance to the social aspect of ESG in their investment approach.[2]

Figure 1. Importance of ESG for institutional investors

The first bonds identified as ‘social’ had the objective of saving the lives of children in poverty around the world by providing them with the necessary vaccinations. These ‘vaccine bonds’ were issued by the International Finance Facility for Immunisation in 2006.[3] They managed to raise more than $4.5bn, a first signal of the great potential of this instrument among investors.

In 2017, the International Capital Market Association (ICMA) published the first guidelines for issuing social bonds, aimed at supporting the development of the market for this innovative financial instrument. The Social Bond Principles (SBP) list the necessary components for a bond to be “certified” as social, namely:

- the proceeds need to be used to finance or refinance social projects;

- the process to evaluate and select projects should be clear and communicated to investors;

- the proceeds must be tracked adequately; and

- issuers should provide investors with an annual report on the use of proceeds.

Furthermore, the SBP list examples of eligible social project categories (e.g., access to essential services such as health and education) and of target populations (e.g., populations living below the poverty line) to provide issuers with some guidance.

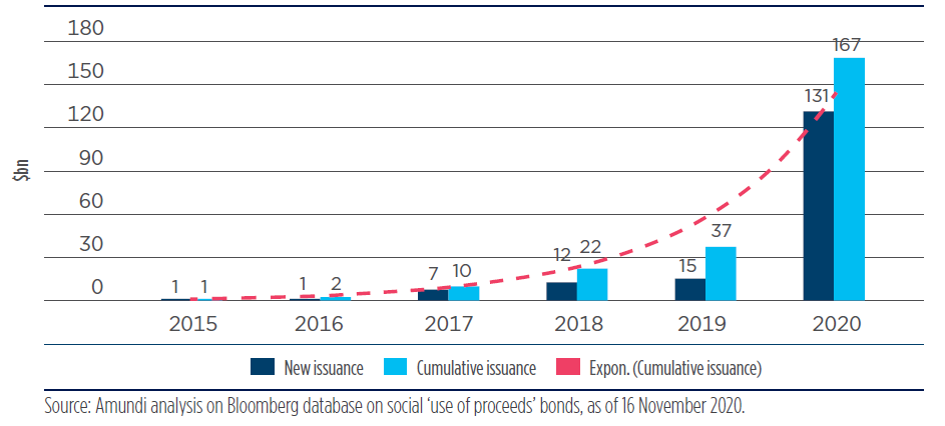

Figure 2. Social bonds market, US$bn

The global social bond market has experienced strong growth in recent years.

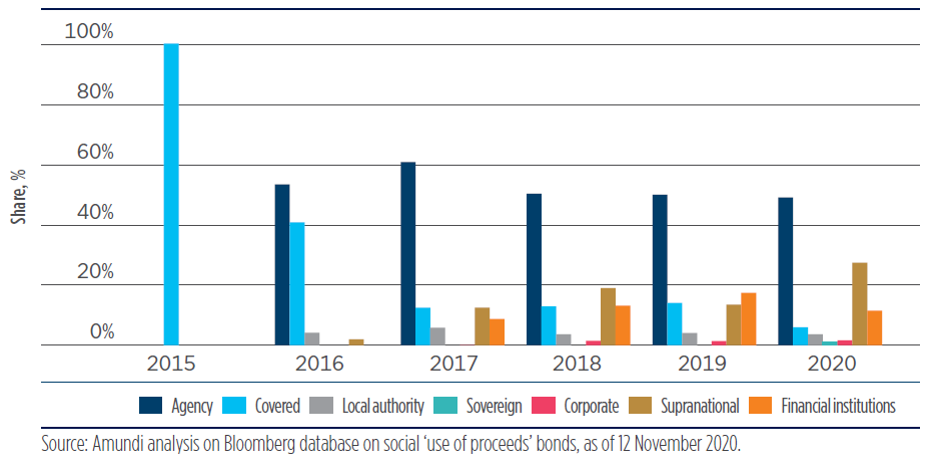

Of the $1280bn in cumulative sustainable fixed income issuance, social bonds account for around 14% of the total, amounting to $180bn.[4] Considering cumulative volumes over the 2015-2020 period, issuance was mainly driven by government agencies (49%), supranational entities (27%), and financial institutions (11%). The over-representation of agencies and supranational issuers is not surprising at this stage of the market’s development as it mirrors the early days of the green bond market.

Figure 3. Issuer type breakdown

In terms of geography, Europe is leading the way, accounting for 45% of new social bond issuance in 2020. However, this share has significantly decreased from 70% in 2017, as issuances in other regions, especially Asia-Pacific and North America, have been rising.[5]

Although Asia has experienced the fastest growth in social bond issuance over the last years, the market is still underdeveloped and Sovereign, Supranational and Agency (SSA) issuers have not been providing a sufficient push yet. In the region, the South Korean government issued the sole social bond of 2019. Nonetheless, last January, India’s Shriram Transport Finance Co. sold a $500m social bond, with the proceeds targeted at truck financing for small and medium enterprises (SMEs).[6]

This overall expansion trend has further intensified during the pandemic. In fact, the growth of the social bond market in 2020, i.e. +374% with respect to 2019 levels, dwarfs both the green and sustainability bonds markets’ expansion, respectively +37% and +100%.[7]

New issuance of social bonds year to date totalled $142bn, more than eight times compared to 2019.[8] This figure does not include the so-called ‘Covid-19 response’ bonds – not completely aligned with the ICMA SBPs – or sustainability bonds with proceeds mostly used for social projects; thus, the total amount of bond issuance with a social focus is even larger than that.

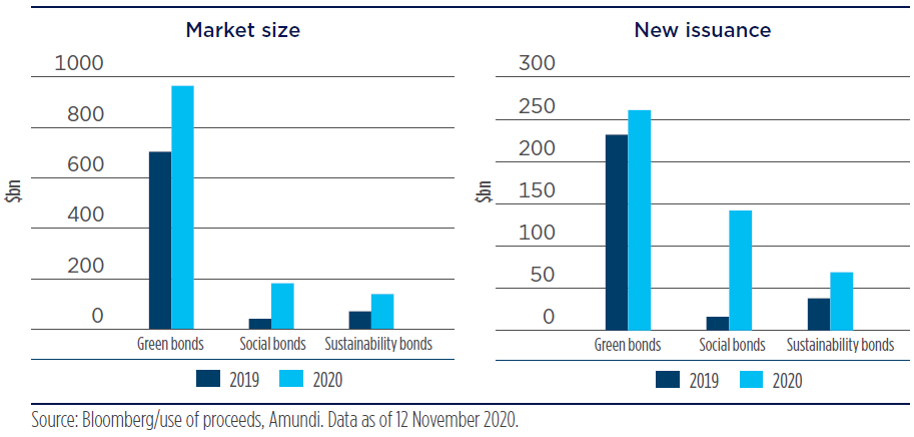

Figure 4. Green, social and sustainability bonds, US$bn

Cumulative social bond issuance remains far below the levels reached in the global green bond market (mere $180bn against $963bn, respectively).[9] However, the crisis has led to a clear expansion across regions of social bond issuances, as these instruments can be used as a tool to respond to a wide range of pandemic-related financing needs.

Social bonds can be the right instruments to respond to the Covid-19 crisis

To guide issuers in this unprecedented period, the ICMA recently published guidelines on resorting to social bonds to finance emergency response measures. Most importantly, the ICMA announced that the Social Bond Principles were immediately applicable to bonds addressing challenges arising from the virus outbreak.

Before the crisis, proceeds from social bonds mostly targeted social housing, support to Small and Medium Enterprises (SMEs), socioeconomic advancement and education programmes.[10] However, in the context of the Covid-19 outbreak, proceeds are expected to be earmarked for a wider range of project categories, such as expenditures to increase capacity in healthcare services and equipment.

Examples of social bonds issued during this crisis include the African Development Bank’s $3bn “Fight Covid-19” social bond in March 2020[11], aimed at alleviating the economic and social consequences of the pandemic on its member countries and the continent’s private sector, as well as the first-ever sovereign social bond issued by the Guatemalan government.[12]

As for the EU, “it is “for the first time in history, […] issuing social bonds on the market, to raise money that will help keep people in jobs” (U. von der Leyen, President of the EU Commission).[13] On October 20, the EU issued its first social bond under the €100bn Support to mitigate Unemployment Risks in an Emergency (SURE) programme. The €17bn social bond was accompanied by a Social Bond Framework, that was assessed to be in line with the four components of the ICMA Social Bond Principles by Sustainalytics’ Second Party Opinion (SPO). The issuance sparked great interest among investors, who oversubscribed it more than 13 times, reaching a record order book of €233bn.[14] According to Refinitiv, it is the highest demand for a bond in history. The second issuance on 10 November was also very successful among investors, with a high degree of over-subscriptions.[15]

Social bonds appear to be an appropriate financing instrument for these times for several reasons. The Covid-19 pandemic has worsened existing social challenges that are affecting the health and well-being of the world’s population. On top of this, the imposed lockdown in most areas of the world and the subsequent global economic crisis it brought about have already impacted millions of people as a result of job losses and social isolation. While social bonds seek to mitigate issues for target populations, they may be beneficial to the general population as a whole in the exceptional context of this global crisis.

As it is the case for green bonds, SSAs can play a role in spearheading the development of the social bond market, which would enable capital to be front-loaded rapidly. According to the Asian Infrastructure Investment Bank (AIIB), at least a quarter of the sovereign bonds issued this year have targeted pandemic-related concerns.[16]

Issuers claim that proceeds from such social bonds will be used to finance the long-term needs of the real economy, and particularly to support healthcare infrastructure investments and provide credit to struggling businesses. As a result, not only can social bonds provide necessary funding during the pandemic, they can also address the aftermath of the crisis and help economies become more resilient to future unexpected shocks. Beyond the current Covid-19 context, social bonds hold immense potential as they constitute adequate tools to meet broader developmental objectives in the decades to come.

The ICMA recently published a document detailing how social bonds – as instruments that channel resources to mitigate major social issues – could contribute to the achievement of the United Nations Sustainable Development Goals (UN SDGs). Some examples of SDGs that social bond financing could address include eradicating world poverty, achieving food security and ensuring the availability of water and sanitation for all. However, the realisation of the SDGs requires massive amounts of capital: according to the UNCTAD’s World Investment Report, the financing gap to achieve the SDGs in developing countries is estimated at $2.5-3.0trn per year.[17] In this context, social bonds could help fill the SDG financing gap, especially since the pandemic could delay the achievement of the SDGs by 10 additional years until 2092.[18]

Why social bonds for institutional investors?

Institutional investors should be interested in social bonds for several reasons.

First, the possibility to finance socially beneficial projects does not come at the expense of returns: in fact, as is the case with green bonds, the risk-return profile of a social bond is in line with that of a regular “vanilla” bond from the same issuer.

While this is normally not feasible with fixed income, social bonds also offer a solid platform for dialogue with corporate issuers. Active ownership, also known as stewardship, is increasingly recognised as one of the most effective strategies to influence issuers to integrate long-term sustainability into their business models and practices. Indeed, by issuing a social bond, the issuer is explicitly committing to using the proceeds for social projects and it is ‘signaling’ to the market its plans to focus its business model on more socially impactful products and services. Thus, it gives an optimal opportunity to investors to put forward an effective engagement strategy while investing in a debt instrument.

Furthermore, issuers are strongly encouraged to provide annually a sufficient level of reporting on the use of proceeds, with the description of the social projects the bonds are financing. This enables investors to report with clarity on their considerations for global social issues and on the measurable social impact their investment is producing. It also decreases the risk of ‘social impact washing’, which can be significant with any investment strategy claiming to produce positive impacts. In order to guarantee the quality of both issuers and issuances, it is vital to facilitate a regular, fruitful exchange and collaboration between the ESG and fixed income teams within large asset managers.

At the current stage of the market, social bonds fit well in a fixed income portfolio as thematic investing. However, the increasing diversity of issuer profiles seems to indicate that the social bond market is starting to follow in the footsteps of the green bond market: thus, social bonds in the future are expected to become an established aggregate fixed income market.

In the meantime, we will focus on the whole social fixed income spectrum by looking also at ‘traditional bonds’ brought to the market by issuers with very strong social practices.

In conclusion, this year’s boom in issuance was brought about mostly by the Covid-19 crisis but has revealed the great potential of social bonds in financing projects with positive impacts for society as a whole. The shake-up caused by the pandemic is expected to support such growth in the aftermath of the crisis and beyond. Thus, long-term investors should consider jumping on the ‘social bonds wagon’ at an early stage to support the development of this innovative instrument and reap the benefits of the expected market expansion away from Europe and SSA issuers and towards more attractive risk-return profiles.

Mots-clés : social bonds – Covid-19 – institutional investors – inequalities – ESG

[1] Amundi (2020) “The Coronavirus and ESG Investing, the emergence of the Social pillar” https://research-center.amundi.com/page/Article/2020/06/The-Coronavirus-and-ESG-Investing-the-emergence-of-the-Social-pillar

[2] https://www.greenwich.com/blog/pandemic-perspectives-part-10-acceleration-trend-toward-esg

[3] ORSE (2019) “Osons les social bonds” https://www.orse.org/nos-travaux/osons-les-social-bonds

[4] https://cib.bnpparibas.com/sustain/social-bonds-the-next-frontier-for-esg-investors_a-3-3005.html

[5] https://www.spglobal.com/ratings/en/research/articles/200622-a-pandemic-driven-surge-in-social-bond-issuance-shows-the-sustainable-debt-market-is-evolving-11539807#:~:text=Social%20Bond%20Issuance%20Has%20Reached%20Record%20Levels,-ICMA%20defines%20social&text=Of%20the%20%24400%20billion%20in,%25%20(see%20chart%201).

[6] https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/asia-pacific-green-bond-issuance-falls-to-over-3-year-low-as-social-debt-surges-60048028

[7] HSBC Global Research (April 2020) “Green Bond Insights – Delayed but not denied.”

[8] Amundi analysis, Bloomberg database on social ‘use of proceeds’ bonds as of November 12, 2020.

[9] https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/social-bond-surge-appears-here-to-stay-as-covid-19-crisis-shifts-funding-needs-58602191

[10] ORSE (2019) “Osons les social bonds” https://www.orse.org/nos-travaux/osons-les-social-bonds

[11] https://www.afdb.org/en/news-and-events/press-releases/african-development-bank-launches-record-breaking-3-billion-fight-covid-19-social-bond-34982

[12] https://www.spglobal.com/ratings/en/research/articles/200622-a-pandemic-driven-surge-in-social-bond-issuance-shows-the-sustainable-debt-market-is-evolving-11539807#:~:text=social%20bond%20market.-,Social%20Bond%20Issuance%20Has%20Reached%20Record%20Levels,%2C%20health%20care%2C%20and%20financing

[13] https://ec.europa.eu/commission/presscorner/detail/en/IP_20_1954

[14] https://www.cnbc.com/2020/10/21/eu-social-bonds-draw-historic-demand.html#:~:text=The%20EU%20makes%20market%20history,demand%20for%20its%20’social’%20bonds&text=The%20demand%20for%20the%2010,for%20the%2020%2Dyear%20paper.

[15] https://www.pubaffairsbruxelles.eu/european-commission-issues-second-emission-of-eu-sure-social-bonds-eu-commission-press/

[16] https://www.aiib.org/en/news-events/media-center/blog/2020/The-Wave-of-Covid-Bonds.html

[17] UNCTAD (2014) World Investment Report https://unctad.org/system/files/official-document/wir2014_en.pdf

[18] https://www.environmental-finance.com/content/news/sdgs-will-not-be-achieved-until-2092-study.html

Isabelle Vic-Philippe is Head of European Aggregate at Amundi. Since joining Amundi in 2004, Isabelle has held several portfolio management positions within the Euro Fixed Income and the Global Multi-Asset teams. Isabelle is also one of Amundi’s prime speakers on the Energy Transition theme internationally. Isabelle began her career at Paribas in 1989 upon completion of a Master's degree in Economics and Statistics from ENSAE (1989) and an MA in Economics from EHESS.

- Social bonds: financing the recovery and long-term inclusive growth - 4 décembre 2020